Most workers are now paying into a pension. But research shows that there is a worrying lack of understanding about how pensions work and why they’re a good option for saving for retirement.

According to Royal London, seven in ten people admit they have little or no knowledge about pensions. Understanding your pension while you contribute can help you get the most out of it and ensure that you understand what it means for your retirement. If you’re unsure about why pensions are used to save for retirement and what happens to your contributions, here are the basics you need to know.

Your pension contributions are invested

The research highlighted that many workers paying into a pension don’t understand what happens to their money.

The money you contribute to a pension is invested. This means the value of your pension can fluctuate depending on investment performance. As you may be paying into a pension for decades, investing aims to help your contributions grow over the long term. As you aren’t making withdrawals from your pension, the returns delivered are invested themselves. This means you benefit from compound growth and your pension can grow even further.

Despite this, just 24% of those with a pension see themselves as an investor. This goes some way to explaining why pension savers aren’t engaging with their investments. Half admitted they have never looked at where their pension is invested. Nearly one in ten (9%) didn’t realise this information was available and 27% didn’t know they could change how their pension was invested.

If you haven’t made any changes, your pension will usually be invested in a default fund. However, pension schemes will offer a variety of funds to choose from. So, it’s worth reviewing these and seeing if alternatives are better suited to your retirement goals. If you’d like some help assessing your pension investments, please get in touch.

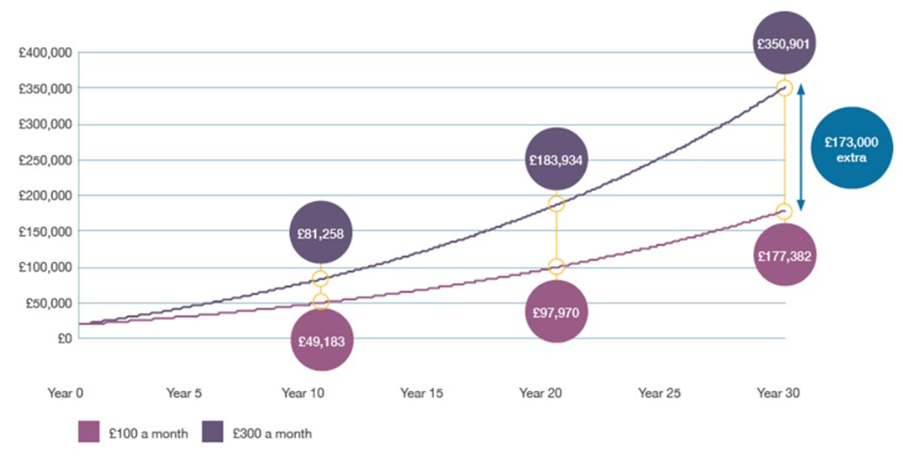

Your employer will make pension contributions

If you’ve been automatically enrolled in a Workplace Pension, your employer must also make contributions on your behalf. This applies to most workers.

The minimum they must contribute is 3% of your pensionable earnings. It can boost your pension and make your retirement more comfortable. However, if you stop making pension contributions, your employer no longer has to contribute either. As a result, you’d effectively lose ‘free money’.

You should review your employee benefits and talk to your employer too. Some employers will increase their contributions in line with yours or offer a salary sacrifice scheme that can provide a tax-efficient way to save more for retirement.

You also benefit from tax relief

The tax relief you receive when saving into a pension means it’s a tax-efficient way to save for retirement.

Assuming you stay within the limits of the Annual Allowance, you’ll receive some of the money you’d have paid in tax on your earnings back to add to your pension. It’s a valuable relief that can boost your pension investments. You receive tax relief at the highest rate of Income Tax you pay.

If you’re a basic-rate taxpayer and want to add £100 from your salary to your pension, it would only cost you £80 thanks to the tax relief. For higher- and additional-rate taxpayers, it’s even more valuable as they’d only need to add £60 and £55 respectively.

Again, if you stopped making contributions, you’d lose this ‘free money’ being added to your pension.

It’s tax-efficient when accessing your pension too

Retirement may still feel like a long way off, but how you’ll access the money you’re saving for this stage of your life is important too. A pension is an efficient way to save for your later years.

First, when you reach pension age, you can take a tax-free lump sum of 25% from your pension. It’s a step that can help you reach retirement goals. You can also choose to spread this tax-saving across withdrawals. At the moment, you can access your pension from the age of 55 but this will rise to 57 in 2028.

While an income taken from your pension may be liable for Income Tax, you don’t usually pay tax on investment returns. The favourable tax treatment of pensions means your pension investments can grow faster.

If you’re worried about Inheritance Tax, saving into a pension could also reduce the eventual bill. Please get in touch with us to discuss further how you can minimise Inheritance Tax.

What does your pension mean for your retirement?

Just as important as understanding how your pension works is knowing what kind of retirement lifestyle it will afford you. Understanding how your pension contributions will add up can help you prepare for retirement and means you’re in a position to make changes if needed. Please contact us to arrange a meeting to go through your pensions and retirement plans.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

A pension is a long-term investment. The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits.

The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation and regulation which are subject to change in the future.

The Financial Conduct Authority does not regulate estate and tax planning.