Our latest guide is in partnership with Neil Bage, founder of Be-IQ, a fintech company focused on behavioural insights. The guide gives a fascinating overview of how our behavioural biases can affect the decisions we make. It could help you better understand your own decisions and what you can do to reduce your biases.

We start with an explanation of what financial biases are and where they come from, as well as looking at ten examples that you may recognise. While bias can influence many financial decisions, from what to spend money on to your relationship with saving money, one of the most researched areas is the impact it has on investing. Our guide explores how bias can sometimes lead you to take too little or too much risk.

Finally, we list some of the steps you can take to reduce your biases when making financial decisions.

If you have any questions about this guide or your financial plan in general, please get in touch.

The current tax year will end on 5 April 2021, a date when many allowances and tax breaks will reset. In some cases, it will be your last chance to use them. Making use of appropriate allowances can help you get the most out of your money.

Our guide explains seven key allowances you should consider to ensure you’re ready for the 2021/22 tax year. This includes:

Keeping on top of allowances and how to use them can be challenging. But creating a financial plan that helps you get the most out of your money can put your mind at ease. Please get in touch to discuss how you can make the most of allowances in the current tax year and put a plan in place for 2021/22.

2020 has been an eventful year for investment markets. Impacted by the Covid-19 pandemic and government responses to this, there have been many valuable investment lessons that will apply in 2021 and beyond.

As the extent of the pandemic became known in March, stock markets around the world suffered sharp falls. In fact, fears of a recession meant the FTSE suffered its biggest fall since the 2008 financial crisis and trading was temporarily suspended on Wall Street as circuit breakers were triggered, according to the Guardian.

Since then, markets have bounced back but continued to experience volatility. The uncertainty of the situation, with governments changing restrictions and support as they try to control the virus, affected markets throughout the summer and autumn.

So, 2020 has been useful in highlighting the investment lessons we should keep in mind.

1. The unexpected does happen

A year ago, who would have predicted that a global pandemic would have occurred? It’s probably not something you’ve ever considered when weighing up investment risks. Yet, it’s had a huge impact on investment volatility and opportunity in 2020.

This year has taught us that the unexpected does happen. We can’t consider every eventuality but preparing for the unexpected can improve your financial resilience. In terms of investing, this may mean having liquid assets or a rainy-day fund you can use if investment values fall. This is particularly important if you’re drawing an income from investments. Having options for when the unexpected does occur should be part of your financial plan.

2. Volatility is part of investing

No one wants to see the value of their investments fall. But volatility is part of investing. When you invest, you need to be aware of the risk that values can fall.

This is why a long-term time frame and goal is so important when investing. Short-term volatility is often smoothed out once you look at investment performance over a longer time frame. It can be frustrating to see that investment values fell in 2020, but when you look at performance over the last five years, for example, you’ll probably still see an upward trend.

3. Diversifying is important

We all know we should diversify our portfolio. Investing in a range of assets, industries and geographical locations can help spread the risk. When one investment falls, another may perform better helping to create balance.

Covid-19 has had a far-reaching impact, with countries around the world affected by the virus. However, some industries have been affected far more than others. Travel and hospitality businesses, for instance, have been forced to close for weeks at a time in many places. In contrast, the pandemic has created opportunities for some firms too. While a balanced portfolio will still have suffered volatility, it can lessen the impact.

4. Financial bias can affect us all

Investment markets have featured in the news more heavily than usual this year, thanks to the volatility experienced. If headlines or talk about the markets meant you considered changing your strategy, financial bias is likely to have played a role.

Financial bias simply means other factors besides facts have influenced your investment decisions. When markets fell sharply at the beginning of the pandemic, an emotional reaction that means you considered taking money out of the markets is normal. However, recognising where bias occurs and limiting the impact is important. Working with a financial adviser can help you with this as you have a professional you trust and one that understands your situation to talk to.

5. You can’t time the market

Finally, the events of 2020 have supported the saying: It’s time in the market, not timing the market.

If you’d tried to guess when to put your money into the stock market and exit this year, you’d probably have ended up making mistakes. Trying to time the market to maximise returns is incredibly difficult, as so many factors play a role. Even investment professionals with a huge number of resources make mistakes.

Rather than trying to time the market, creating a long-term plan and sticking to it is usually the most appropriate strategy for investors.

What to expect in 2021

So, what lies ahead for the next 12 months? With lockdowns and restrictions continuing around the world, we expect further investment volatility as we head into 2021. But if 2020 has taught us anything, it’s that we can’t predict what’s around the corner. Think about your aspirations and build a long-term financial plan around these, including investing where appropriate.

Please get in touch if you’d like to review your investment portfolio for the year ahead.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

‘New year, new me,’ goes the common saying. The start of a new year is often seen as a time to reinvent yourself and make plans towards goals. With 2020 causing so many setbacks and challenges, you may be thinking about setting a new year’s resolution to start 2021 on track.

While setting a new year resolution is common, less than one in ten ends up sticking to them. So, whether you want to exercise more, learn a new skill or make lifestyle changes, setting out a plan can improve your chances of success. If you want to make changes in the new year, here are seven tips to help you achieve your goal.

1. Focus on one thing

When you’re feeling motivated and want to make changes to your life, it can be tempting to make sweeping changes in one go. But good habits can be hard to form. Deciding to hit the gym three times a week, increase your savings and learn a new language on the same day can set you up for failure.

Rather than transforming your whole life, pick an area you want to focus on and work towards this goal. You can always add other aspirations once positive habits have been formed with your first resolution.

2. Be realistic, but make it a challenge

Setting a target is the first challenge of sticking to a new year’s resolution. Make it too easy and you can lose focus, but make it too difficult to achieve and you can lose motivation. You need to be able to realistically reach your goal in the space of 12 months but also ensure that the resolution will have a positive change in your life, encouraging you to keep at it.

Make sure your goal is measurable too. Rather than a vague idea like ‘I want to save more’, set a plan to save a certain amount each month.

3. Break your overall goal into smaller chunks

A new year’s resolution can be daunting when you look at it as a whole. Breaking down a wider goal into smaller segments can help you remain positive and focused throughout 2021. For instance, if you’re hoping to lose weight in the coming year, set monthly targets as well as an end-of-year goal.

It’s a process that can make even larger goals seem more manageable and reduce the chances of you giving up because the final target seems out of reach. Remember to make sure these smaller goals are realistic too.

4. Chart your progress and celebrate your successes

Keep track of your progress towards your goals too. Whether you choose a traditional pen and paper or an app, having your progress noted down can help you get through those times when you’re finding it a challenge. Looking at the hard work and progress you’ve already made can be enough to push you to keep going.

Remember to celebrate when you make progress too. If you’re working up towards running a marathon in 2021, completing that first 5k if you don’t usually run is a milestone. Planning treats for yourself when you reach certain points can help keep you on track.

5. Enlist the help of family and friends

A support system can make all the difference when we’re striving towards goals. Letting family and friends know your plans means they can help you towards your target.

If they’re also working towards the same or similar goal, having a buddy to do it with can make it far more fun and add some friendly competition into the mix. But even if this isn’t the case, loved ones can be valuable support when you feel like giving up. Sometimes, someone giving you a bit of encouragement or even tough love can be enough to boost your motivation, so you keep going.

6. Learn from the past

Have you made new year’s resolutions before? You probably have at some point. By taking some time to review why they were successful and unsuccessful, you can find a way of working that’s right for you. There’s no ‘right’ way to work towards a goal, but by understanding why you’ve given up or didn’t meet expectations in the past, you can set out a plan that matches your mindset.

7. Don’t give up when you slip up

Finally, making long-term changes is hard and good habits take time to stick. Even the most dedicated can experience a setback. Don’t let a small slip up knock you completely off track. It can be frustrating, but look at why you’ve missed a target and learn from it. Finding a way to keep going when things don’t go to plan is often the difference between success and failure.

If you’re setting financial goals this year, please get in touch. Whether you want to save more, start investing or plan your retirement, we can help you incorporate these into your financial plan to set a path for success.

Stock markets in 2020 have been characterised by volatility and uncertainty. If you’ve made financial decisions based on your feeling towards this, it could have cost you money.

Whenever we make a decision, we have to weigh up the different options. While reasons and facts should be the basis for any decision you make, emotions play a role too. Where this happens when making financial decisions, this is called financial bias. It can mean you end up making decisions that aren’t appropriate for you.

In recent months, as markets have experienced volatility and economic uncertainty has featured in the news, this may have affected the decisions you’ve made too.

Moving to cash due to Covid-19 cost investors 3%

According to behavioural finance experts Oxford Risk, investors that responded to Covid-19 uncertainty by moving more of their wealth into cash could have missed out. By switching to cash for ‘emotional comfort’ it’s calculated that investors have missed out on returns of 3% or more a year.

Separate research also suggests that investors moved more of their wealth into cash in response to Covid-19. In the first half of 2020, UK households put away £77 billion in cash, taking the total amount saved in cash accounts to £1.5 trillion. While a cash account to cover emergencies is advisable, it’s estimated that nearly £1.2 trillion of this cash isn’t needed for contingencies.

With cash accounts currently offering low-interest rates, it’s estimated that UK households have missed out on £38 billion in potential investment returns.

While investing does come with risk, it can help your money grow at a faster pace than when using a savings account. However, you need to invest with a long-term time frame, a minimum of five years. This provides an opportunity for short-term volatility to smooth out. Investing for a short period means there’s a higher chance that you could lose money due to short-term downturns.

There are many reasons investors held more of their money in cash during the first half of this year. But for some, financial bias will have played a role.

For example, information bias occurs when investors evaluate information, even if it doesn’t relate to their situation. It makes it difficult to assess what information is relevant. The sheer amount of information can be overwhelming. During the pandemic, investors have been bombarded with news, forecasts and opinions about what will happen. With much of this coverage negative, it’s natural that some investors will have had an emotional reaction and decided that cash was safer.

Trying to time the market provides an opportunity for financial bias

It’s not just a trend that is having an impact due to Covid-19 either. When the markets are performing well, it can be tempting to increase how much of your wealth is invested. In contrast, it’s common to want to move your money to ‘safety’ at times when markets are performing poorly or experiencing volatility.

However, this can mean you end up buying assets while prices are high and selling at low points. Oxford Risk estimates this type of financial bias can cost investors an average of 1.5% to 2% a year over time. Over a long-term investment strategy, financial bias can end up costing you significant sums.

While it can be tempting to move money in and out of investments to maximise returns, trying to time the market is difficult. As the above averages show, you’re more likely to miss out on returns than to increase your portfolio’s value. For most investors, a long-term investment strategy is appropriate.

Minimising financial bias: Stick to your long-term plan

Creating a long-term plan based on your goals and sticking to it can help you minimise the impact of financial bias. That can be easier said than done, though, especially at times of uncertainty. Working with us can help you here. A financial planner will be able to help you understand your long-term financial positions and act as a second pair of eyes when you want to make changes. It can mean financial biases can be highlighted and discussed.

That doesn’t mean you should never make changes to your financial plan. After all, circumstances and goals do change, and your financial plan may need to change to reflect this. However, this should be driven by long-term aspirations and be based on evidence.

Please contact us, if you’d like to go through your financial plan and investment strategy.

Please note: The blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Most workers are now paying into a pension. But research shows that there is a worrying lack of understanding about how pensions work and why they’re a good option for saving for retirement.

According to Royal London, seven in ten people admit they have little or no knowledge about pensions. Understanding your pension while you contribute can help you get the most out of it and ensure that you understand what it means for your retirement. If you’re unsure about why pensions are used to save for retirement and what happens to your contributions, here are the basics you need to know.

Your pension contributions are invested

The research highlighted that many workers paying into a pension don’t understand what happens to their money.

The money you contribute to a pension is invested. This means the value of your pension can fluctuate depending on investment performance. As you may be paying into a pension for decades, investing aims to help your contributions grow over the long term. As you aren’t making withdrawals from your pension, the returns delivered are invested themselves. This means you benefit from compound growth and your pension can grow even further.

Despite this, just 24% of those with a pension see themselves as an investor. This goes some way to explaining why pension savers aren’t engaging with their investments. Half admitted they have never looked at where their pension is invested. Nearly one in ten (9%) didn’t realise this information was available and 27% didn’t know they could change how their pension was invested.

If you haven’t made any changes, your pension will usually be invested in a default fund. However, pension schemes will offer a variety of funds to choose from. So, it’s worth reviewing these and seeing if alternatives are better suited to your retirement goals. If you’d like some help assessing your pension investments, please get in touch.

Your employer will make pension contributions

If you’ve been automatically enrolled in a Workplace Pension, your employer must also make contributions on your behalf. This applies to most workers.

The minimum they must contribute is 3% of your pensionable earnings. It can boost your pension and make your retirement more comfortable. However, if you stop making pension contributions, your employer no longer has to contribute either. As a result, you’d effectively lose ‘free money’.

You should review your employee benefits and talk to your employer too. Some employers will increase their contributions in line with yours or offer a salary sacrifice scheme that can provide a tax-efficient way to save more for retirement.

You also benefit from tax relief

The tax relief you receive when saving into a pension means it’s a tax-efficient way to save for retirement.

Assuming you stay within the limits of the Annual Allowance, you’ll receive some of the money you’d have paid in tax on your earnings back to add to your pension. It’s a valuable relief that can boost your pension investments. You receive tax relief at the highest rate of Income Tax you pay.

If you’re a basic-rate taxpayer and want to add £100 from your salary to your pension, it would only cost you £80 thanks to the tax relief. For higher- and additional-rate taxpayers, it’s even more valuable as they’d only need to add £60 and £55 respectively.

Again, if you stopped making contributions, you’d lose this ‘free money’ being added to your pension.

It’s tax-efficient when accessing your pension too

Retirement may still feel like a long way off, but how you’ll access the money you’re saving for this stage of your life is important too. A pension is an efficient way to save for your later years.

First, when you reach pension age, you can take a tax-free lump sum of 25% from your pension. It’s a step that can help you reach retirement goals. You can also choose to spread this tax-saving across withdrawals. At the moment, you can access your pension from the age of 55 but this will rise to 57 in 2028.

While an income taken from your pension may be liable for Income Tax, you don’t usually pay tax on investment returns. The favourable tax treatment of pensions means your pension investments can grow faster.

If you’re worried about Inheritance Tax, saving into a pension could also reduce the eventual bill. Please get in touch with us to discuss further how you can minimise Inheritance Tax.

What does your pension mean for your retirement?

Just as important as understanding how your pension works is knowing what kind of retirement lifestyle it will afford you. Understanding how your pension contributions will add up can help you prepare for retirement and means you’re in a position to make changes if needed. Please contact us to arrange a meeting to go through your pensions and retirement plans.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

A pension is a long-term investment. The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits.

The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation and regulation which are subject to change in the future.

The Financial Conduct Authority does not regulate estate and tax planning.

Global stock markets continued to be affected by Covid-19, but there was good news mixed among the negative.

While the International Monetary Fund (IMF) warned the global economic recovery was ‘losing momentum’, markets rallied during the month based on the news that a vaccine was on the way. Pfizer was the first to announce a vaccine, closely followed by AstraZeneca. While it could be some time until a vaccine allows us to return to normal, it’s a light at the end of the tunnel.

UK

Throughout much of November, the UK was in a second lockdown, fuelling fears of a double-dip recession.

In line with these concerns, the Covid-19 furlough scheme was extended until March 2021 to protect jobs and businesses.

The Chancellor also delivered his Spending Review, which sets out plans for the 2021/22 tax year. The statistics painted a gloomy picture. The government is now borrowing at its highest level in peacetime history and the economy is predicted to shrink by 11.3% this year. The new year isn’t expected to bring relief either. Unemployment levels are forecast to reach a peak of 7.5% in the second quarter of 2021 and the economic output isn’t expected to reach pre-crisis levels until the end of the year.

Unsurprisingly, shares in UK travel companies, pub chains, retailers and hotel operators all fell sharply with the news of a second lockdown. Among those affected were:

Wetherspoons (-7%)

Whitbread, owner of Premier Inn (-3.7%)

JD Sports (-5.8%)

IAG, parent company of British Airways (-6.3%)

A survey conducted by the Office for National Statistics also highlighted the challenges businesses are facing. One in seven companies (14%) fear they will not last until next spring. This sentiment was particularly high among hospitality firms.

Not all firms have been negatively impacted by lockdown through. Some, such as supermarkets, takeaway delivery firms and DIY retailers, saw stocks rise.

The Bank of England has also commented on another risk to businesses – Brexit. The central bank warned that disruption caused by firms being unready for the transition period with the EU coming to an end will shave 1% off growth in the first quarter of 2021.

Europe

Looking to the EU, it is again a mixed bag of good and bad news.

Eurozone GDP increased by 12.6% in the third quarter. However, investment bank Goldman Sachs predicts economic growth will be negatively affected by the new restrictions across Europe. As a result, the bank expects the European economy to shrink again in the final quarter of 2020 and warned this is a trend that could continue into 2021.

Technology companies have largely been resilient during the Covid-19 volatility but that doesn’t mean they’re ‘safe’. In November, the EU hit Amazon with anti-trust charges over merchant data. Following an investigation by the European Commission, Amazon has been charged with distorting competition in the online retail sector. A second investigation is also pending. The firm faces a potential fine as high as 10% of its global turnover, about £15 billion.

US

The big news from the US in November was, of course, the presidential election. Uncertainty over who had won and whether legal action would be taken led to volatility in the markets in the days following the vote. However, the markets did enjoy a Biden bounce as it became clear that Joe Biden will be the 46th President of the United States.

While the US still battles to control Covid-19, headline figures suggest the economy is recovering at a stronger pace than expected. According to the Institute of Supply Management, US manufacturing grew at its fastest pace in almost two years in October. Output was 59.3, compared to the 55.8 forecast on a scale where a reading above 50 signals growth.

This was also reflected in the unemployment rate dropping to 6.9%, down from 7.9% in September.

Asia

In Asia, there were also positive signs of recovery, but fears remain. Japan was the latest country to exit a recession after posting 5% growth in the third quarter. However, concerns that the country now faces a third wave of Covid-19 dampened the news.

Moving away from Covid news, the largest technology firms in China saw the value of their shares fall sharply this month. Beijing’s market regulator took its first major step in tackling the monopolistic power of tech giants. E-commerce firm Alibaba was one of those affected, with shares falling 9%.

Keep up to date with market and financial news by keeping an eye on our blog. Please get in touch if you have any questions about your investments or financial plan.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

The start of a new year is the perfect time to get your finances in order.

A few simple changes could improve your finances in 2021 and beyond, setting you up for a healthier financial future.

So, whether your finances are in a muddle or you just want to ‘do better’, here are five new year’s resolutions worth sticking to.

1. Create a spending budget

If your bank balance has been getting worryingly low, it’s probably time to take a thorough look at your spending habits.

Creating a budget is a useful exercise whatever stage you’re at in life. And you may be surprised at how easily you’re able to save extra money each month.

The following simple steps can help you create a successful budget:

Work out how much money you take home each month

Add up your monthly outgoings

Calculate the difference

If your expenses are greater than your income, check if there’s anything you could cut back on. We’re not suggesting you scrap all of your little luxuries. However, there may be lots of things you’re spending money on that you don’t actually need, such as unused magazine subscriptions or gym memberships.

If your income is higher than your outgoings, consider adopting the ’50-30-20’ budgeting philosophy. This is where essential expenses comprise half your budget, other expenses make up 30%, and the remaining 20% goes towards savings or paying off debt.

2. Pay off expensive debt

If you’ve racked up a lot of debt, the new year could be a great time to start tackling it.

The higher the interest rate, the more the debt will cost you, so it’s usually a good idea to pay off expensive debts first. These could include credit card and store card debts, unauthorised overdrafts, and payday loans.

Paying off your debts could enable you to save more money for your future, improve your credit score, and reduce any anxieties you’re feeling about your finances.

Some loans come with high early repayment penalties, so make sure you read the terms and conditions before paying them off.

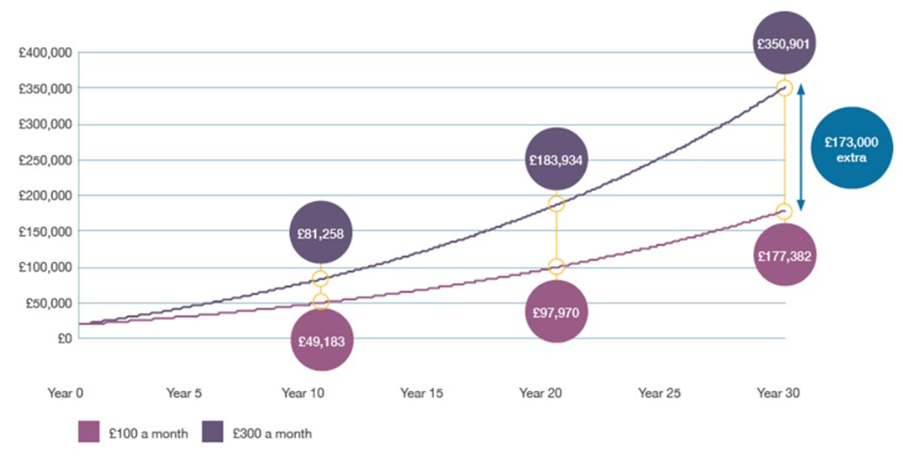

3. Increase your pension contributions

If you’ve got extra money sitting around or recently received a pay rise, it could be worth increasing your pension contributions.

Each time you pay into a pension the government tops it up with 20% tax relief, making it a great way to save for your future.

The chart below shows how quickly monthly pension contributions can add up over time. It shows two £20,000 pensions growing by 5% a year over 30 years. One has £100 paid into it each month, and the other has £300.

It’s never too late to start preparing for your future. However, the earlier you start investing, the better your chances are of living the retirement you desire.

Research by Which? suggests couples need £27,000 a year to live a comfortable retirement, or £42,000 a year to live a luxury retirement that includes a holiday every year and a new car every five years.

Couples would need a pension pot of around £215,450 to produce enough income for a comfortable retirement via income drawdown, or £298,000 through a joint-life annuity. For a luxury retirement, these figures rise to £502,775 and £695,000, respectively.

4. Invest in a Stocks and Shares ISA

Investing in a Stocks and Shares ISA has several benefits. Your money grows free of Income Tax and Capital Gains Tax, and you can withdraw money whenever you like without paying tax.

This makes ISAs a useful vehicle for holding money that you might need to withdraw before retirement. Money inside a pension can’t be accessed until you’re at least 55-years-old, rising to 57 in 2028.

Additionally, because ISA withdrawals are tax-free, they can be a tax-efficient way of taking income in retirement. With a pension, you can withdraw up to 25% tax-free and the rest is taxed at your marginal Income Tax rate.

You can pay up to £20,000 into ISAs in the 2020/21 tax year. Keep in mind that when investing, your capital is at risk. You should invest with a minimum five-year timeframe in mind.

5. Make a will

Making a will is an essential financial exercise, yet research by Royal London suggests 57% of UK adults don’t have a will in place.

If you die without a will, it could cause immense stress and financial hardship for your family. In a worst-case scenario, your loved ones could inherit nothing and become embroiled in bitter disputes.

By making a will, you can ensure:

Your money and assets end up in the right hands

Your children are cared for by people you know and trust

Your unmarried partner and stepchildren are provided for

Your family can continue living in their home

Your estate doesn’t attract unnecessary Inheritance Tax

Writing a will can give you the peace of mind that your loved ones will be protected long after you’ve gone.

Get in touch

If you want advice on getting your finances in order, we can help. From helping you create a financial plan to organising your pensions and other assets, we’ll ensure your new year is off to a flying start. Please contact us to arrange a meeting.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

A pension is a long-term investment. The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation and regulation which are subject to change in the future.

The Financial Conduct Authority does not regulate will writing or estate and tax planning.

How many times have you told yourself you are going to try and save more but then somehow several months slip by without putting away a penny? You’ve paid for everything else – rent or mortgage, shopping, bills, clothes, holidays and maybe even a few meals or nights out but you haven’t paid your most valuable asset – you. And so it goes on and on. This happens to everyone, regardless of income level. If this sounds familiar, it could mean you should change your mindset and pay yourself first.

This is not the same as spending money on yourself! It’s saving some money before you do anything else. This is setting aside a certain portion of your income the day you get paid before you spend any ‘fun money’. I’m not being a kill joy here, quite the opposite. This is me trying to help you prolong joy! Many people wait and only save what’s left over—that’s paying yourself last. What this could ensure is that one day, you finish the rat race without the cheese.

Understand your current self

Take a look at yourself. I mean your life as a whole – what do you enjoy doing? What are your hopes, loves, hates, fears, habits, routine, family etc. This is your current self. Your current lifestyle is funded by your current self.

Now have a think about what you would like your future self to be. Do you imagine much will be the same? What would you want to be different? Many people imagine a more comfortable future, perhaps a continued or better lifestyle. Most certainly don’t want to give up any of the luxuries they may have become accustomed to. The problem is that we are sometimes very optimistic creatures that don’t think about the bridge between the current and the future. How are you going to pay for that future? ‘It’ll be alright’ is a path that surely won’t end well.

Pay your future self

So, one of your current self’s main responsibilities is to fund your future self. This can be achieved by the practice of paying yourself first, helping to make sure your future self’s key financial goals are covered, including building up an emergency fund, contributing to retirement and saving for any other long-term goals, like a bigger home. You should be your biggest bill. The bottom line is that it’s important to have all of these things covered before you spend your hard earned pounds on that flash car, slap up meal or top of the range phone.

According to a recent report by Legal & General, the average UK household only has enough savings to last 32 days, before hitting the breadline. Around 15% of people in the UK have no savings at all. Individual circumstances obviously make a difference, but one this is certain – we are living longer and the responsibility of funding our lifestyle, for life, is our own. According to Aegon in their 2018 retirement readiness report, 59% of people in the UK think that future retirees will be worse off. About 22% think that it will be around the same. The way that many people behave, I’d have to agree with the 59%!

Our unique opportunity

You’d think this would be enough to scare most people into saving better, except there’s the little matter of, well, just about everything else that payday has to cover. This is why we are all currently in a unique position to break the cycle. Coronavirus is unfortunately spreading at a faster rate once more, meaning more lockdowns and less opportunity to spend money on a day to day basis. Use this to your advantage!

The sooner you get started, the better off you may be. Not only will you be able to take advantage of compound growth (more on this later) to help grow your money faster, but you’ll also help ensure that your financial goals are getting funded before life happens. Don’t wait too long or the car might break down, the boiler might break, you might spend too much of your spare time on Amazon or the pubs might re-open until a reasonable hour!

Saving should be automatic

Switching to a ‘pay yourself first’ mentality can be hard because people don’t like change. We are a stubborn stuck in our ways bunch. It’s like challenging the status quo. That’s why rather than physically having to make the decision to do this every month it’s absolutely the best idea to make this automatic. Take the slice of your income that you have decided you want (need!) to pay your future self and pay this automatically into the right investment.

Set up a direct debit to your pension or ISA before you see that money hitting your current account. Paid on the 1st? Great set the direct debit to that day. Even better, if your savings are for retirement then your employer may be able to divert your pay directly to your pension. This may include extra matched contributions from them if you are lucky.

This is a marathon not a sprint

The hard bit here is that you are not going to get instant gratification. You should not over do it, as you will be more inclined to stop. You should not under do it, or your future self will be skint. With the right amount of automatic, forgotten about, steadily increasing savings you will be surprised how much you can pay your future self. long term saving is slow and boring! I promise you though, this is worth it to ensure you don’t have to be boring in the future too.

How much you choose to save will depend on your current budget and your desired lifestyle both now and in the future. If you don’t have a budget you damn well should have! I recommend, as soon as possible, going through the pain of getting your last three months statements and analysing them thoroughly. All you need is a pad, pen (or spreadsheet), a cuppa (substitute for beer/wine only after 4.30pm Friday) and an hour. That’s it. Your task in this time? To know exactly what your spending looks like. What is fixed or flexible, essential and non essential. Simple as that. Just this task alone will highlight the stark reality of your current self. You may feel satisfaction. You may feel shame.

Either way, if you think you are not saving enough, finding the costs you can reduce or eliminate is key. Because you are either saving or spending money. There is no inbetween. The grey area that your mind thinks exists between the two is non existent – like the exercise you do with the gym membership you haven’t used in a while. What you save by trimming the cost of stuff such as this is all money that can be used to pay yourself first.

What could making this choice do for me?

A lot. The table below shows the amount you would be paying your future self after saving a monthly amount for 10 years. There are three rates of return. Why? Because if you are saving for a few years you should definitely be considering your options for bettering bank rates. This is ample time to ride out the ups and downs from stock market returns. You should take the opportunity to grab your fair share of profit made by the companies you support through your spending every day. This doesn’t have to involve lots of risk and if this is something you don’t understand you can take some advice – I promise this will be worth it. Find out what you could save each month and take a look below at what you could potentially achieve. This might be a surprise for you!

10 year saving example

£’s Saved per month

3% Return

5% Return

7% Return

£100

£13,974

£15,528

£17,308

£200

£27,948

£31,056

£34,616

£300

£41,922

£46,584

£51,925

£400

£55,896

£62,112

£69,233

£500

£69,870

£77,641

£86,542

£600

£83,844

£93,169

£103,850

£700

£97,818

£108,697

£121,159

£800

£111,793

£124,225

£138,467

£900

£125,767

£139,754

£155,776

£1,000

£139,741

£155,282

£173,084

Capital accumulated after saving monthly for 10 years with three rates of return

What if I’m self employed?

Anyone who owns their own business knows the ups and downs of good and bad months, I know this from personal experience. It’s harder to save a specific amount when you don’t know how much you’ll make from month to month.

So how do you deal with this?

Dead easy. Your budget should be based on an average month. Businesses should be thought of as seperate to personal finances. Your business may be cyclical, but as with any financial planning exercise this is about taking away uncertainty. Putting some money aside in the good months, will ensure that there is always capital to pull so that you can pay yourself first.

Of course, this only works if business owners are paying themselves a salary to begin with. Many small business owners tend not to pay themselves at all—let alone first. Often they leave as much in the business account as they can, reducing their salaries to nothing. This can sometimes be counter productive. You have yourself to look after as well as your business.

In summary

The ultimate guiding principle behind paying yourself first putting your own long-term well-being ahead of almost every other financial situation – because you are your own biggest asset. All this being said though, it’s just another way to look at the process of getting together a long term financial plan. At the end of the day, financial planning is all about the current and the future.

If all this sounds good it’s time to take action. If you’d like some help to formulate the plan, give me a shout – I’ll be happy to help build your wealth and future happiness.

Don’t make your future self hate your current self. Just pay yourself first.